Why Every Landlord Needs Robust Landlord Insurance: More Than Just a Safety Net

Could you afford to lose nearly half your rental income to tenant damage or a household nightmare? Most landlords could, and often do, when relying on standard home insurance. Without robust landlord insurance, one fire, flood, or malicious act could wipe out your profits overnight. A specialist policy ensures you’re never left exposed...

For most landlords, their rental property isn’t just an asset, it’s a livelihood. Yet, many underestimate how fragile that livelihood can be without the right protection. While standard household insurance may seem sufficient, it often leaves landlords dangerously exposed.

A robust Landlord Insurance policy - like the one we provide through our partnership with Goodlord - offers far more than peace of mind; it offers protection that truly fits the realities of renting.

Standard Household Insurance is not enough

Regular home insurance is designed for owner-occupiers. It assumes the person living in the property is the one who owns it, meaning it doesn’t account for the unique risks of letting to tenants. Here’s what standard home insurance often doesn’t cover:

❌ Tenant-related damage (malicious or accidental).

❌ Loss of rent if the property becomes uninhabitable.

❌ Public or property owner’s liability if a tenant or visitor is injured.

❌ Alternative accommodation costs for tenants during repairs.

In other words, a normal household policy might protect the bricks and mortar, but not the business of being a landlord.

The Importance of Landlord Insurance

Landlord insurance bridges those gaps. It protects your income, your reputation, and your property investment from tenant-related risks and unexpected disasters. Without it, you could lose up to 45% of your annual rental income through damage and repairs, as shown in industry research cited by Goodlord.

A robust landlord insurance policy should include:

✅ Buildings cover for up to £1,000,000 (for fire, flood, subsidence, theft, and malicious damage).

✅ Property owner’s liability up to £2,000,000.

✅ Loss of rent or alternative accommodation cover if the property becomes uninhabitable.

✅ Accidental and malicious damage cover, including tenant damage.

✅ Optional contents cover for furnishings and gardens

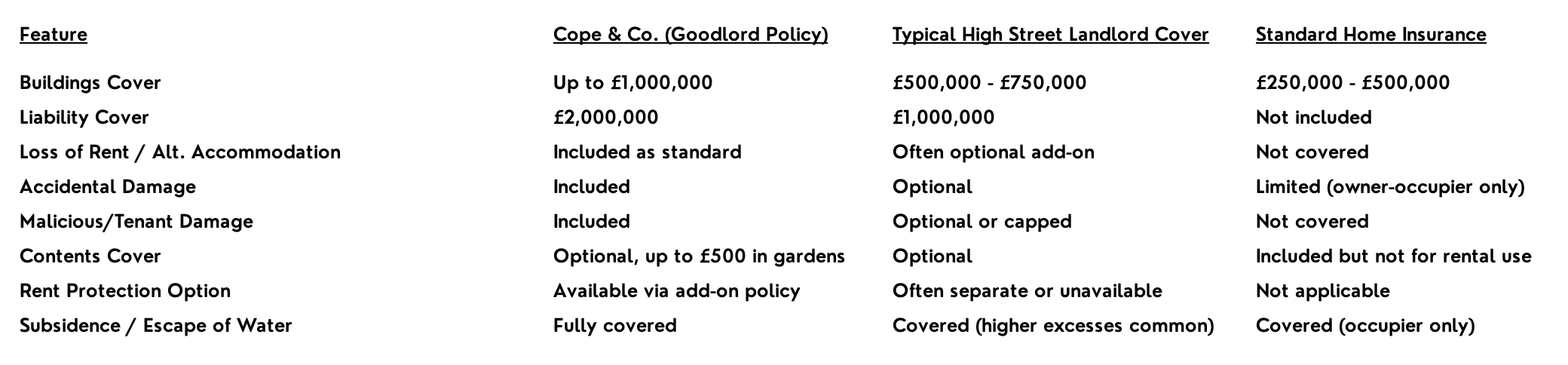

Cope & Co. Landlord Insurance vs. High Street Competitors

Unlike most high street offerings, our policy is purpose-built for landlords, combining both building and content protection with optional add-ons like Rent Protection Insurance for arrears

.

Why Our Cover Stands Out

Beyond the numbers, it’s the design of our cover that makes it robust. Where some insurers charge extra for essentials, our policy provides comprehensive coverage as standard; including for events like tenant vandalism, subsidence, and alternative accommodation.

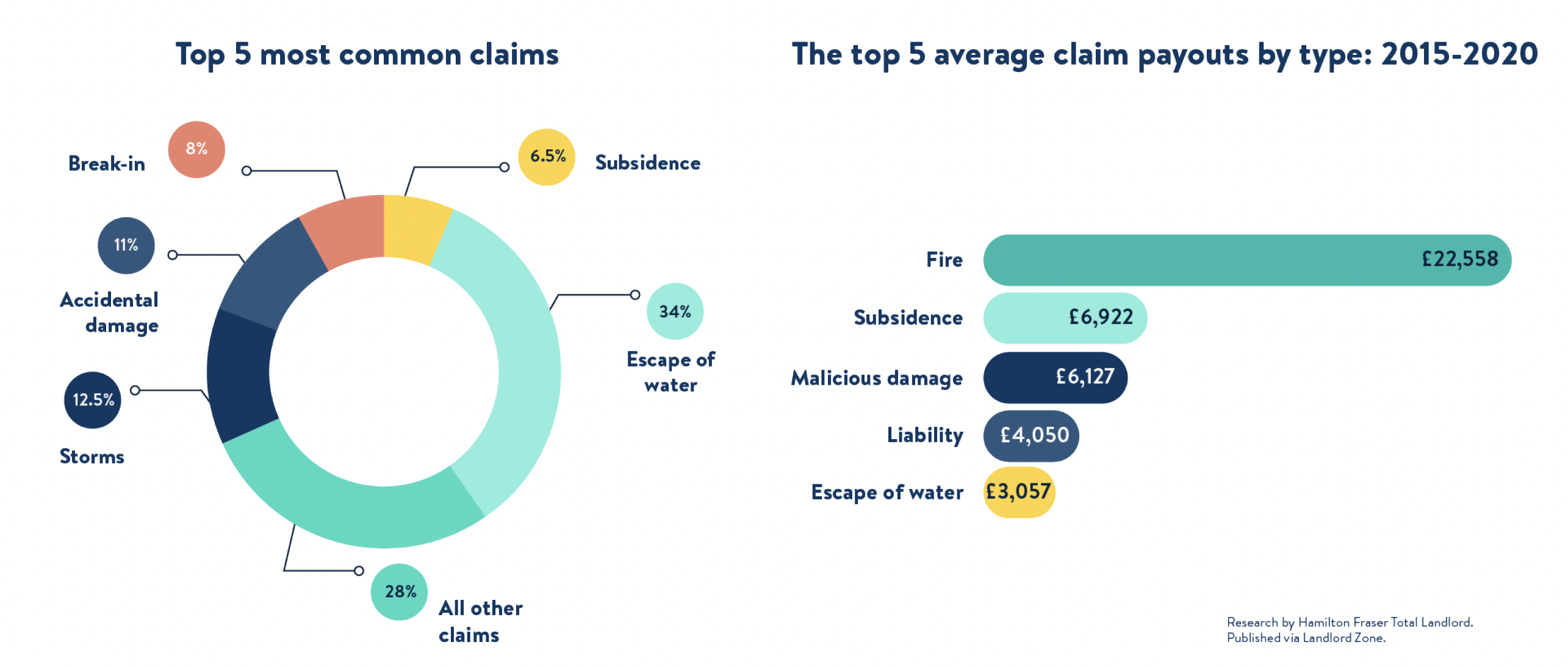

The data also speaks volumes. According to the chart below, escape of water and storms are among the most common claims, while fire has the highest average payout at over £22,000. This shows why a well-rounded policy is vital: one event could cost more than several years of insurance premiums combined:

The Bottom Line

For landlords, protecting your investment isn’t just about repairing bricks and mortar, it’s about ensuring continuity, income stability, and professional credibility. A robust landlord insurance policy keeps your property business resilient, compliant, and ready for anything.

With Cope & Co.’s Landlord Insurance, you’re not just insured, you’re protected, prepared, and partnered for peace of mind.

Contact me today and see how our specialist landlord insurance can get you covered.